Most home buyers and sellers do not realize that the total costs of closing a real estate transaction are more than double the Realtor commissions. So, let me explain how much money it really takes to buy or sell a house. Seeing who gets the money and how much will surprise you. You will also find out which fees are negotiable and which are firm.

A few weeks ago my husband and I spent time analyzing the settlement statement (HUD-1) of a recent closing. It was a simple, $90K home purchase with bank financing and only 3% in real estate commissions.

As we reviewed the statement line by line we were surprised to see a variety of new fees. Surprisingly we find that the total cost of closing this real estate transaction was approximately 12% of the purchase price.

Let’s Look at the Settlement Statement

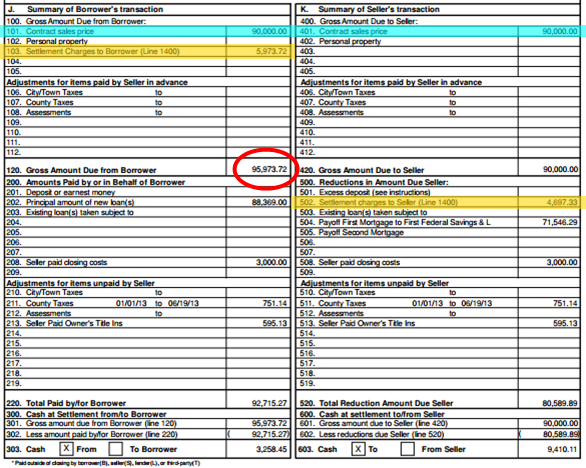

In the left upper box on page 1 of the settlement statement you can see the total cost of the home purchase – $95,973 in our case. The Buyer/Borrower’s closing costs amount to $5,973, approximately 6.6% of the purchase price.

The Seller’s portion of closing costs – in the right lower box – adds up to $4,697 (5.2% of the purchase price, with only 3% in real estate commissions.)

The total costs of a real estate transaction are commonly split between the buyer and the seller. The seller usually pays the majority of the title and transfer fees. The buyer is responsible for items that relate to the financing of the purchase (loan fees).

The total costs of a real estate transaction are commonly split between the buyer and the seller. The seller usually pays the majority of the title and transfer fees. The buyer is responsible for items that relate to the financing of the purchase (loan fees).

The buyer and seller may negotiate how the fees will be split. For instance, the seller may pay some of the buyer’s closing costs – $3,000 in the statement above – to reduce the amount of cash the buyer needs to bring to closing..

Itemized Closing Costs

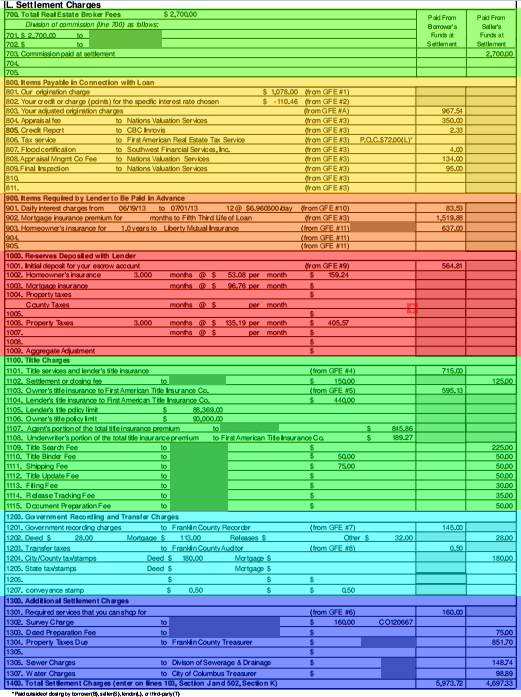

The itemized costs of closing a real estate transaction are shown on page 2 of the settlement statement. Let’s have a look at the different types of fees you will find on your settlement statement. Here’s a sample settlement statement, color coded by different categories of fees.

Real Estate Broker Fees

The first line item shows the real estate commissions. They are typically 6% of the purchase price. The brokerage directly receives the commission (not directly to your agent). They are split between the buyer’s agent and the listing agent, usually 3% each. However, commissions are somewhat negotiable. Occasionally, you see them as low as 4% or as high as 7%.

In this example only one side of the commission was charged at 3% of the purchase price.

Items Payable in Connection with the Loan

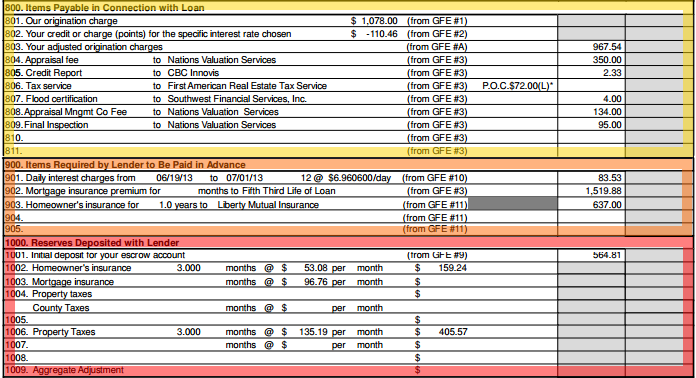

The first section in the picture above (yellow) itemizes the fees associated with originating the loan for your home purchase. There are items that go to your lender, your mortgage broker or the bank. Other items include fees for pulling your credit report and to complete the appraisal.

You may notice that the appraisal fee is $350 in this sample. However, the buyer was charged additional fees for appraisal management ($134) and a final inspection ($95).

These are mostly fixed fees, although loan origination may be a percentage of the loan amount. They are somewhat negotiable with your lender, e.g. you may lower your origination fees in return for a higher interest rate.

Lender Requires You to Pay in Advance

Your lender requires the pre-payment of certain items (orange), such as Mortgage Insurance and Home Owner’s Insurance (for the first year). They also charge interest on your loan from the day of closing to the first of the next month.

The good news is that your first mortgage payment won’t be due until the end of the following month. Interest is always paid in arrears, so you skip a mortgage payment when you sell your house and buy a new one.

These items depend on the loan amount or purchase price and are not negotiable.

Reserves Deposited with Lender

It’s not enough that you have to pay your insurance in advance. Your lender also wants to establish an escrow to make future insurance and property tax payments (red). Typically, you have to deposit 3 months worth of payments in the escrow account.

These items are variable depending on your insurance and interest rates, and not negotiable.

However, some lenders do not escrow insurance and property taxes. In that case it is up to you to make these payments when they are due. You only pay principal and interest every month.

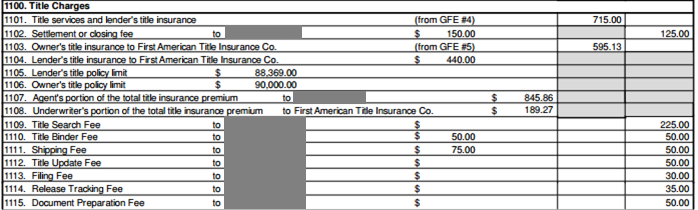

Title Charges

The next big block of fees covers items paid to the title company. There are 3 parts:

- The settlement fee is paid to the title company for handling everything related to the physical closing of the home purchase.

- Title search related fees are charged for examining the title to the property and providing title insurance for the owner and the lender.

- The Title Policy fee itself, is an insurance premium that guarantees you have good and marketable title. There’s a policy for the owner and there’s one for the lender.

With the exception of the title policy, which is variable based on your purchase price, the other fees are fixed and set by the title company. While the policy premiums are non-negotiable and the same anywhere in Ohio, all other title fees are negotiable.

Savings Tip 1: As a seller you should always keep your existing title policy, as the title company will only charge a re-issue rate which is 10% – 30% less expensive than a new policy.

Savings Tip 2: Title charges vary widely dependent on the title company. Ask your real estate agent for the company with the lowest fees and the best service.

The seller usually selects the title company. As a buyer you may have less leverage for negotiating fees, however, most of the time the seller pays for the title fees.

Government Recording & Transfer Charges

This is where the government gets its share of the real estate transaction. There are 2 types of fees:

- Recording Charges are paid to the county for recording the deed and the mortgage in the public records to document your ownership and to secure the mortgage. These fees are fixed (per page) and, obviously, not negotiable.

- Transfer Fees are like a sales tax you need to pay to the county auditor for transferring ownership of your property. Transfer fees are based on the purchase price and not negotiable.

Additional Settlement Charges

Here you will find all kinds of miscellaneous fees. Take a good look at this section and make sure that the fees are justified. Ask the title company why certain fees are there.

In our sample you can see a survey fee, a charge for deed preparation, property taxes that just became due, as well as unpaid water and sewer charges.

Charges Outside of Closing

Keep in mind that not all costs of a real estate transaction are show up on the settlement statement. Some expenses the buyer or the seller directly pay outside of the closing (these items on the HUD-1 have a POC mark). Other expenses, like a home inspection, doesn’t show up on any official records.

Benefits of Working with a Realtor

All these fees may sound confusing.

But this is how to make sure the realtor doesn’t overcharge.

By how much will these fees reduce your payout at closing?

There’s no need to worry, if you work with a professional Realtor.

Your real estate agent can help you negotiate fees and show you how to keep them low.

Before you list your house the agent will create a “net-sheet” that shows exactly how much you will net at closing.